“You better start swimming, or you’ll sink like a stone. Because the Time’s they are a-changing.” – Bob Dylan (from the song)

I have long been an advocate of enterprise organizations giving themselves a makeover, albeit a calculated one, by building out an elastic,flexible and agile IT operation in areas of the business that demand such innovation. Gartner has a popular moniker for this – “Bimodal IT”.

And then I read this article today morning about BofA bringing in 60% of all it’s sales from Digital Channels. Behold that! A staggering 60%! I reproduce the below snippet directly from the article..

Bank Of America might want to change its name to Digital Bank of America.

The Charlotte, N.C., megabank is more digital bank than conventional financial institution today. That’s because 60% of the bank’s “sales” are “all digital now,” Brian T. Moynihan, Chairman and CEO of Bank of America, told investors yesterday.

Moynihan also disclosed that about 6% of the bank’s digital “sales” – it is difficult to identify exactly what he means by “sales,” unfortunately – are via mobile device, “and that’s growing at 300%,” he said.

Moynihan’s disclosures yesterday were the most publicly detailed on digital banking at a major bank to date.

Ref – http://bankinnovation.net/2015/07/share-of-digital-sales-at-bank-of-america-hits-60/

BofA have been in the news the past couple of years whether that be about incubating OpenStack into their next generation architecture and innovative use of data & mobile technology in areas where they need to attract a critical, fast growing & coveted segment of the population – millenials. It is unclear if the digital portion is being wholly run out of this open source based infrastructure but we can draw some valuable object lessions from a technology strategy perspective.

To paraphrase the above point, how does such an approach boil down in terms of technology principles? And pray, what are the technology ingredients that make up a successful Digital Strategy or more importantly how do all the principles of webscale apply at a large organization? I would wager that there are five or six major factors, chief among them – an intelligent approach to leveraging data (ingesting, mining & linking microfeeds to existing data – thus a deep analytical approach based on predictive analytics and machine learning), an agile infrastructure based on cloud computing principles, a microservice based approach to building out software architectures, mobile platforms that accelerate customers abilities to Bank Anywhere, an increased focus on automation both from a business process to software system delivery and finally a culture that encourages risk taking & a “fail fast” approach.

Lets examine each of these forces in turn, starting with Cloud Computing first.

It may safely be said that the first wave of cloud computing adoption or Cloud 1.0 is largely a mainstream endeavor in industries like financial services and no longer an esoteric adventure meant only for brave innovators. A range of institutions are either deploying or testing cloud based solutions that span the full range of cloud delivery models – IaaS (Infrastructure as a service), PaaS (Platform as a service), SaaS (Software as a service) etc . Cloud has moved beyond proof of concept into production.

Figure 1 – IT is changing from service provider to service partner

As Brett King notes in his seminal work on Digital Banking a.ka Bank 3.0, this is the age of the hyper-connected consumer. Customers are expecting to be able to Bank from anywhere, be it a mobile device or use internet banking from their personal computer.

Thus there is significant pressure on Banking infrastructures in three major ways –

- to be able to adapt to this new way of doing things and to be able to offer multiple channels and avenues for such consumers to come in

- offer agile applications that can detect customer preferences and provide value added services on the fly. Services that not only provide a better experience but also help in building a longer term customer relationship

- to be able to help the business prototype, test, refine and rapidly develop new business capabilities

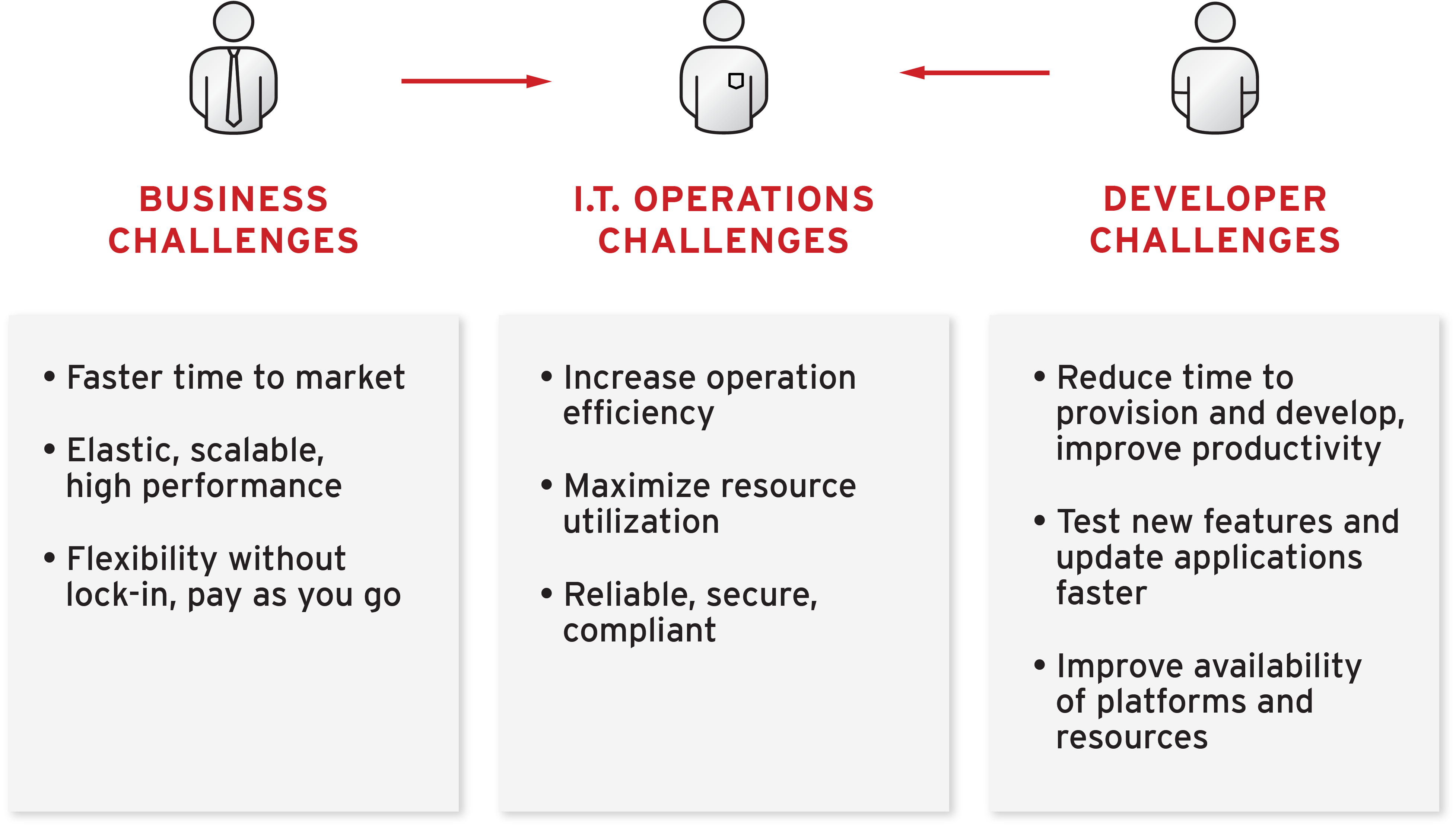

The core nature of Corporate IT is thus changing from an agency dedicated to keeping the trains running on time to one that is focused on innovative approaches like being able to offer IT as a service (much like a utility) as discussed above. It is a commonly held belief that large Banks are increasingly turning into software development organizations.

|

Figure 2 – IT operations faces pressures from both business and line of business development teams

The example of web based start-ups forging ahead of established players in areas like mobile payments is a result of the former’s ability to quickly develop, host, and scale applications in a cloud environment. The benefits of rapid application and business capability development has largely been missing in the with Bank IT’s private application platform in the enterprise data center.

|

Figure 3 – Business Applications need to be brought to market faster at a very high velocity

None of the above has to mean increased cost both from an IT and manpower standpoint. The worlds leading web properties and Fortune 1000 institutions use a variety of open source technologies ranging from Hadoop to OpenStack to PaaS to Operating Systems & Virtualization. Robust and well supported offerings are now available across the spectrum and these can help cut IT budgets by billions of dollars.

Not entirely convinced of the value proposition? Reproduced below are some other metrics for Bank of America’s digital banking for last quarter (from the same article):

- Bank of America has around 17.6 million mobile users, about 14% more than in the second quarter of 2014;

- 13% of deposit transactions via mobile; and

- 10,000 appointments scheduled via mobile device a week, up from 2,000 a year ago.

Ref – http://bankinnovation.net/2015/07/share-of-digital-sales-at-bank-of-america-hits-60/

The next post in this series will focus on Big Data and it’s global role in all aspects of banking by helping organizations mine the gold that is customer data (at a minimum).

We will look at business imperatives & usecases across seven key segments – Retail & Consumer banking, Wealth management, Capital Markets,Insurance, Credit Cards & Payment processing, Stock exchanges and Consumer Lending. My goal will be to talk about how the Hadoop ecosystem can not just satisfy existing usecases (yes, the ubiquitous datawarehouse augmentation) but business requirements across a spectrum and finally helping adopters build out Blue Oceans (i.e new markets).